What is disability insurance? Does your current insurance policy cover it? Keep reading this well-researched article on insurance.

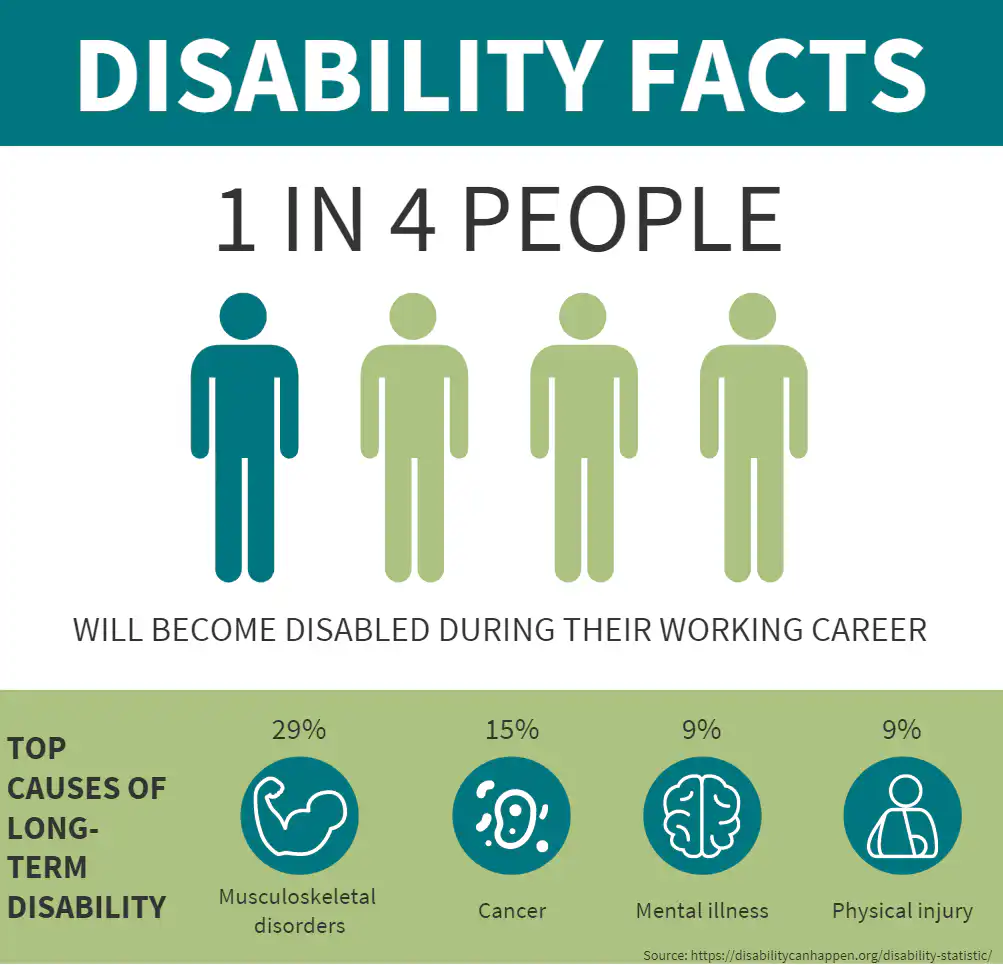

Research has proven that one out of every four workers will become disabled during their working life. That person could be you. Will you have insurance coverage if this misfortune happens to you?

Again, 29% of workers suffer disability related to Musculoskeletal, another 15% may suffer cancer, 9% suffer mental illness while another 9% get messed up by one physical injury or the other. Clearly the future is uncertain for today;s worker.

What would happen if you lost your job, couldn’t work because of illness or injury, or failed to meet some other life-changing obligation? Unless you have a trust fund or a family member willing to bail you out, you might need insurance to help pay for expenses while you recover.

Insurance is not just for the rich; it’s also for people with common sense. After all, who wants to be left with nothing when something goes wrong?

Luckily, there are different kinds of insurance – including insurance against loss of income as the result of illness, disability or old age – that can protect your future in case something unfortunate happens.

Keep reading to find out more about this type of insurance and whether it may be right for you.

What is disability insurance?

Disability insurance is insurance that pays you a regular income if you become disabled and can’t work.

Some types of disability policies also may pay you a lump sum if you become disabled and are unable to work long enough to qualify for Social Security disability benefits.

Disability policies are often sold as “disability income” policies, but disability insurance is not the same thing as disability income insurance. For most people, disability insurance is a good idea since not everyone is able to save enough money in case of an emergency.

In addition, most people will become disabled at some point in their lives.

Your risk of becoming disabled increases as you get older, so it’s important to purchase disability insurance when you’re young.

How does disability insurance work?

Disability insurance works much the same way as life insurance.

You pay a regular premium, and the insurance company promises to pay a specified benefit if you become disabled.

When you apply for disability insurance, you will be required to take a medical examination.

The purpose of the exam is to determine whether the insurance company should accept you as a policyholder.

In most cases, you will not be turned down for coverage if you have been in good health and have a good work history.

The insurance company will charge you a lower premium or provide a larger benefit if you have a condition that makes it less likely that you will become disabled.

The company also might charge you a higher premium or provide a smaller benefit if you have a condition that makes it more likely that you will become disabled.

Thus, if you have a health problem that could interfere with your ability to work, you will want to be sure to inform the insurance company about your condition.

Why is Disability Insurance Important?

Disability insurance is important because it can help you replace your lost income if you cannot work due to an injury or illness. When you are healthy, most people don’t think about disability insurance. After all, there’s no point in paying for insurance that you don’t need.

However, if you can’t work because of a serious illness or injury, you may need insurance to cover your living expenses until you are able to work again.

Short-term disability insurance typically covers you for a period of six months or less.

Long-term disability insurance typically covers you for a period of two or more years. Most disability insurance policies pay a benefit that is equivalent to a percentage of your pre-disability income.

How much coverage you should buy is a good question.

The amount you should purchase depends on your financial situation, your family’s financial needs, and the amount of coverage you are likely to receive from the government.

How to buy Disability Insurance?

You can buy disability insurance through an insurance agent or broker, through an insurance company’s website, or directly from an insurance company by phone.

Since disability insurance is a type of insurance, you’ll need to ask several questions before buying a policy.

These questions include: how much coverage you need, how much coverage is available, how much it will cost, and what type of policy best meets your needs.

If you want coverage immediately, you can purchase a single-disability policy.

If you want coverage that will take effect (be payable) after a specified number of months, you can purchase a group long-term disability policy.

READ: How to attain the American dream as a foriegner in America

Final Words: Know when you should get Disability Insurance

There are many types of disability policies, each with different features and benefits. Before you buy a policy, be sure to understand what the policy covers and how much it will cost you each month or annually.

When you are young and healthy, it makes sense to buy a long-term disability policy that will protect you if you become disabled and unable to work.

However, long-term disability policies are more expensive than short-term policies since they provide more coverage for a longer period of time.

If you can’t afford long-term disability insurance, you can buy short-term disability coverage.

Disability insurance protects you from financial hardships if you become unable to work.

It is important to buy disability insurance when you are young since you are more likely to become disabled as you get older.

Disability insurance is not something most people think about until they need it.

The good news is that many people qualify for disability insurance through their employers.

If you don’t have coverage through work, you can buy a disability insurance policy on your own.

With disability insurance, you can provide for your family’s daily needs and protect your long-term financial security in case something unexpected happens.

[wp-rss-aggregator]